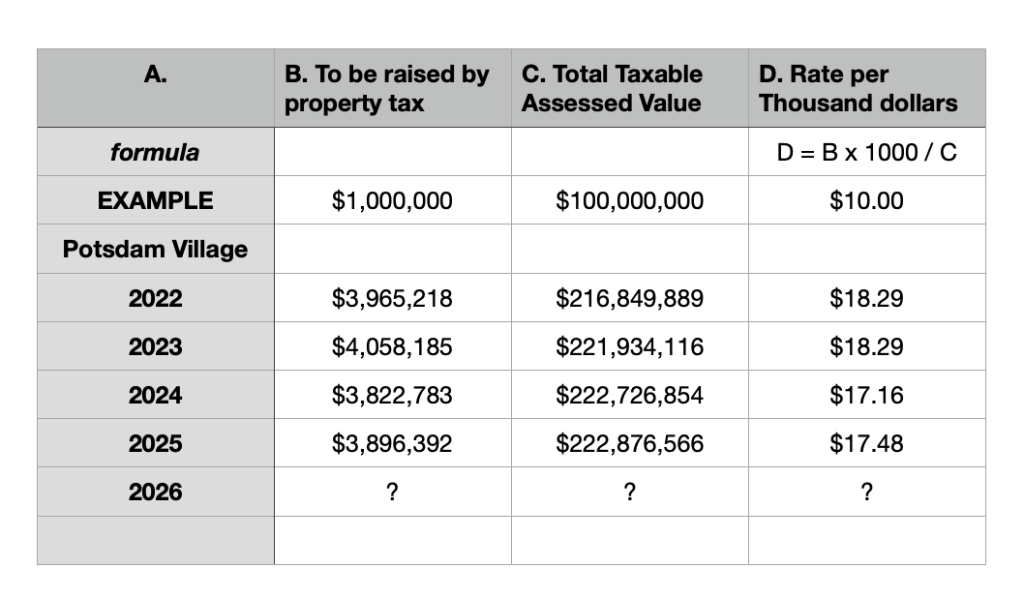

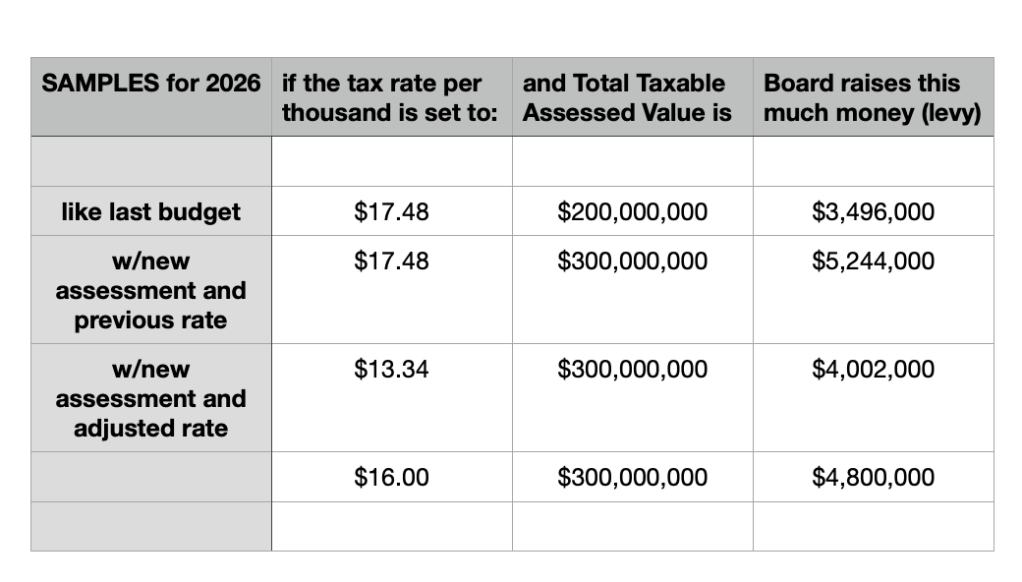

From Albany’s Times Union daily newspaper, an article dated May 20, 2025 by Nora Mishanec demonstrates the troubles local municipalities get into. While this article pertains to a town of 9,800 in the mid-Hudson valley, the details sound very familiar:

PLEASANT VALLEY — Residents of Pleasant Valley may have overpaid in taxes for years after a state audit of town finances found that the town’s board did not develop realistic budgets or properly manage its money.

The audit of the Dutchess County town of 9,800, released this month by the state comptroller’s office, determined that Pleasant Valley’s five-member town board consistently underestimated tax revenue and overestimated expenses from 2019 to 2023, resulting in a $6.4 million budget surplus.

The budgeting flaws over that period “may have placed a higher tax burden on taxpayers than necessary to provide services,” according to the report.

The report noted that town officials “generally agreed” with the findings and would take steps to correct the imbalances noted in the audit. Supervisor Mary Albrecht, the chief executive and financial officer responsible for the town’s day-to-day financial operations, did not respond to a request for comment. Albrecht was appointed to the board in 2019.

“While the audit focuses on past practices, I believe the steps we’ve taken demonstrate a clear course correction and commitment to continual improvement,” Deputy Supervisor Michael Rifenburgh, who joined the board in 2022, said in an email.

New board members had “worked diligently to deliver responsible and transparent fiscal planning” in the three budget cycles since the audit, Rifenburgh said. Under new leadership, the town tax rate “decreased by approximately 17% and total budgeted expenses have dropped to 2022 levels — despite inflationary pressures, rising personnel costs, and the lingering impacts of the COVID-19 pandemic.”

The largest budgeting errors appeared to have occurred during the 2021 fiscal year, when town officials estimated they would receive about $400,000 in sales tax but brought in more than $1 million. That same year, officials estimated collecting about $100,000 in mortgage tax but received quadruple that amount. The discrepancies, auditors noted, reflected that the board “did not consider historical or known revenues and expenditure trends when preparing annual budgets.”

The town’s two main operating funds each accumulated millions in budget surpluses. Property and sales taxes collectively generated an operating surplus of $5.1 million for the town’s general fund, while the highway fund’s surplus exceeded $1.2 million. Town officials “lacked a plan on how the funds (would) be used,” auditors said, adding that “there was no rationale” for accumulating such significant sums.

“As a result, the board maintained real property taxes at a level higher than necessary for operations and missed opportunities to lower real property taxes,” according to the report.

Town officials told auditors that they had not updated their budgeting practices from prior years and agreed to improve budget estimates by considering historical trends.