Water and sewer rates have been adjusted to reward water conservation: If you currently use less than 40 gallons per day (gpd) you will pay less than previous years while if you use more than 40 gpd you will pay more. (40 gpd translates to 1,200 gallons per month or 4,000 gallons per quarter)

I use around 6,000 gallons/quarter so I pay a bit more than last year.

While the rate change encourages water conservation and gives people some control over expenses, it’s likely to create a financial crunch for the village: Most of the water and sewer departments expenses are not tied to water use, but to salaries and debt payments not tied to water use. Expect W/S rates to be adjusted annually as we continue to try to balance the financial constraints of households and businesses against the expense of operating state-of-the-art water and sewer plants.

The village boundary was once a square 2 miles by 2 miles, encompassing 2,560 acres. Additional lots have been incorporated: Clarkson University added 415 acres around the water tower trail. The Price Chopper, Lowe’s and the Mayfield apartment lots added another 131 acres around outer Market St. The airfield beyond Hatch Rd. added a further 256 acres. So the village boundary currently encompasses a bit over 3,100 acres.

How much of this land is in private hands and taxable?

The river removes 316 acres from development.

What other properties are tax-exempt? Clarkson University’s 640 acres. NY State’s 240 acres of the SUNY Potsdam campus. The Potsdam village municipality owns the 80 acres of the 3 Potsdam Central School District schools. Potsdam village altogether owns 313 acres (a large fraction of that being the airport). The Town of Potsdam owns about 15 acres of village land. Rochester Regional Health, between its Canton Potsdam Hospital Leroy St campus as well as its Lawrence Ave campus, owns 36 acres.

Other nonprofits with significant landholdings include Bayside Cemetery Association, with over over 71 acres, the Potsdam Housing Authority with 18.7 acres at Evergreen Park on the Racquette Rd and the Midtown Apartments with 2.6 acres. Mayfield Apartments sit on 13 acres. Other nonprofits with smaller holdings include The Church of Latter Day Saints with nearly 4 acres, our two Baptist churches with a bit over 8 acres and Trinity on Fall Island with 3.2 acres. NYSUT occupies 2 acres. When you sum the land owned by these various nonprofits, it totals to nearly 1,450 acres.

How many acres do our roadways occupy? Analyses indicate that roads take up between 18-30% of urban land. If we assume a low 15% of land to be taken up by roads on the original 2 by 2 square miles, this subtracts another 384 acres from development.

How many acres of land remain that are taxable? Of the 3100 acres, no more than 954 acres are currently taxable. Or slightly less than 31%.

If we prefer to look at the actual value of the lots, rather than acreage: The total assessed value of taxable lots (tax rolls 1, 5, 6 and 7) in FY23 came to $223 million. The total assessed value of all nonprofits came to $459M. So the fraction of the total assessed value that contributes to the tax base is 223/(223+459)=33%. That this fraction is slightly larger than the acreage fraction is perhaps due to the fact that roadways are not assigned assessed values.

These numbers, while stable, are not fixed. The 5-member village board of Trustees can vote to classify and re-classify the Property Class Code of every parcel in the municipality. Places of worship may be established, federal, state or county-supported low-income housing can be created, hospital and university campuses may expand and the town/village line may occasionally be redrawn (as for the Airport Diner recently).

Nonprofits provide valuable and laudable services that appeal to visitors and residents alike. Without our famous landmarks, Potsdam would be a very different place. But the nonprofits, in turn, require a robust tax base to finance the departments of public works, police, civic center, recreation, as well as debt payments, salaries, health insurance and retirement benefits for current and former employees and their dependents. Given that our municipality can obtain no tax revenue from more than 2100 of our 3100 acres, should the administration continue to cede parcels to the nonprofit sector? The annual ask (appropriations) of the village’s General Fund went from $6.5 million in fiscal year 2022 to $7.5 million in 2024, a 15% increase. Sales tax revenue has also increased, but not enough to keep our tax rate level. Is it therefore in the residents’ interest to cede land via sale (as we did with a portion of Cottage St) or via permanent easement of residential land (as was just done with the 2 acre lot at the end of Clough St)? Unless a reliable alternative revenue source for the General Fund is identified, I would advise caution in relinquishing more land to the wholly exempt section of our tax rolls.

According to a village Trustee, Potsdam village has a 20% commercial vacancy rate. Not only downtown, but also on outer Market street storefronts stand empty – think of the former Ponderosa (closed in 2020), Walgreens (closed this year), Dominos, Sears and Monro Muffler, among others. Potsdam’s Monro Muffler left a sign on its door in 2020, stating, oxymoronically: “We’re moving to serve you better! Come Visit Us in Nearby Locations” and then listing their locations in Canton and Massena. That made me curious: why did the Potsdam Monro Muffler get shuttered and not the ones in Canton or Massena? Why did the Potsdam Walgreen shutter, and not the Walgreen’s in Canton? Are stores in Potsdam somehow at a disadvantage?

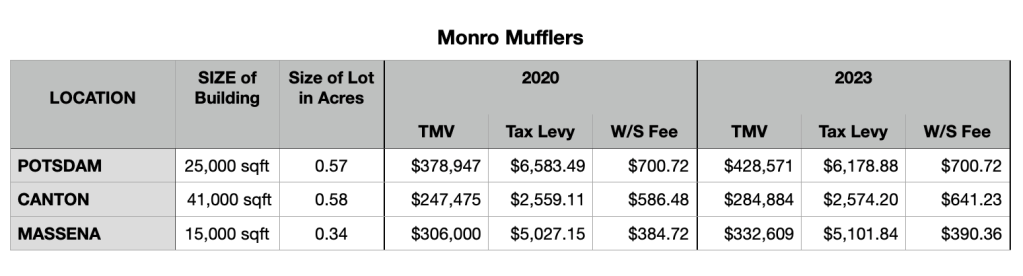

In an effort to put some numbers in place, I searched the St. Lawrence County online data-base, looking up assessed or Total Market Values (TMV) of the 3 Monro Mufflers. The online data-base also reports the property taxes paid by each location, annually. Finally, I inquired about each municipality’s water and sewer taxes/fees. I tabulate results below. The numbers show that operating a business in the village of Potsdam costs significantly more than operating the same businesses in our neighboring municipalities.

Monro’s in Potsdam and Canton each occupy nearly 0.6 acres while Massena’s is situated on a smaller 0.3 acre lot. Monro’s in Canton has the largest store-size, at 41,000 square feet, followed by Potsdam’s with 25,000 square feet and then Massena’s with 15,000 square feet. Oddly, the store with the largest square footage and biggest acreage had the smallest assessed or Total Market Value! Canton’s Monroe Muffler had an TMV of just under a quarter million dollars in 2020. Massena’s Monro Muffler’s TMV was higher, at $300,000 while Potsdam’s Monro’s ranked first with a TMV of nearly $380,000 in 2020.

The assessed values or TMV of properties increase over time, as seen in the table below. There is no pattern to the increases. The Monro Muffler in Massena suffered no increase in its TMV from 2019 through 2022, then it increased by 9% in 2023. The TMV of Monro Muffler in Potsdam increased 2% from 2019 to 2020, then increased 1% in 2021, 4% in 2022 and 7% in 2023, even though this location no longer served customers and sits idle since 2020. The Monroe Muffler in Canton, meanwhile, had a 10% increase in its assessed value in 2021 and a further 5% increase in 2023. There seems to be no rhyme or reason to the increases in TMV across the 3 municipalities.

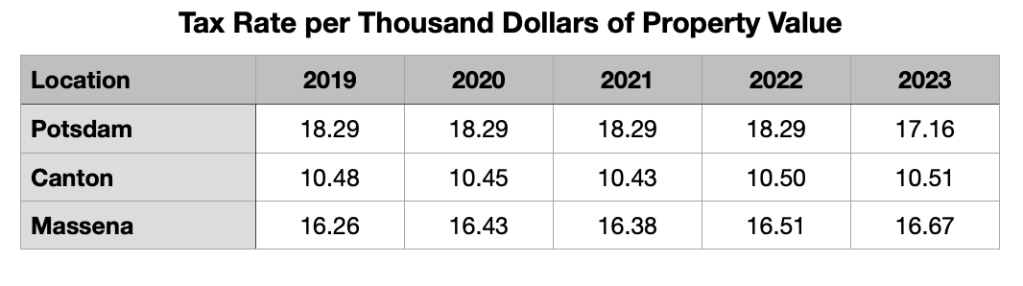

How did the tax levies compare? In 2020, when Monro was still operating in Potsdam, Canton’s Monro Muffler paid by far the smallest property tax, at under $2,600; Massena’s Monro paid a bit over $5,000 in village taxes; while Potsdam’s Monro Muffler had to pay nearly $6,600 in village taxes. This is concerning, as the village of Potsdam drew down its General Fund reserve by a quarter million dollars in 2023 in order to lower its tax rate that fiscal year by over $1 per thousand dollars in property value (see chart below). In spite of that, Potsdam’s Monro Muffler still paid two-and-a-half times more in village taxes than its larger store in Canton in 2023-2024. The Potsdam store also paid 20% more in village taxes than the Massena store last year.

What about the Water and Sewer Taxes / Fees? Let’s assume that each establishment uses 43,800 gallons of water and sewer per year. (Why 43,800 gallons? Because that amount of water-use equates precisely to 1 EDU in Potsdam, and is a reasonable estimate for annual water-use in an establishment.) In this expense category, water and sewer fee, Potsdam businesses also pay the most: Monro in Potsdam pays $700 in water and sewer fees; Monro’s in Canton pays a bit under $600 for identical water and sewer use, while Monro in Massena pays under $400 for its water and sewer fees.

In sum: Potsdam’s Monro has the highest assessed value, even though it neither has the largest lot nor the biggest nor the most modern store. Potsdam also has the highest tax rate of all three municipalities, averaging over $18 per thousand dollars of property value, nearly twice as high as the tax rate in Canton and also higher than in Massena. Combine the higher tax rates with higher assessed values, and businesses end up paying significantly more in taxes in Potsdam than the neighboring municipalities. Finally, for the same amount of water use, businesses in Potsdam again pay nearly twice the water and sewer fees as in Massena, and also more than in Canton.

Are these the reasons the Monro Muffler in Potsdam shuttered while the ones in Canton and Massena still operate? Why the Potsdam Walgreen’s closed, but not Canton’s Walgreen’s? Does our tax structure deter, perhaps prevent, businesses with small profit margins from succeeding in our municipality, i.e. businesses like clothing and shoe stores and small food retailers? Might our tax structure instead favor business models that either pay no property taxes, like college and medical campuses, or businesses that employ high sales volume model, such as the chain stores Lowes and Price Chopper, or businesses with more robust profit margins, like restaurants?

Since commercial establishments pay the same tax rates as private residences, can we infer that private residences also pay lower taxes in Canton? Yes. And indeed, as discussed in a previous post, during the previous decade the population of the village of Potsdam decreased 12% while the population of the village of Canton increased by 13%. Businesses and homeowners will likely continue to shift locations to lower their expense burdens as disposable incomes shrink. Our lower-tax neighbor will continue to act as a black hole for Potsdam, pulling people and resources into its sphere of influence.

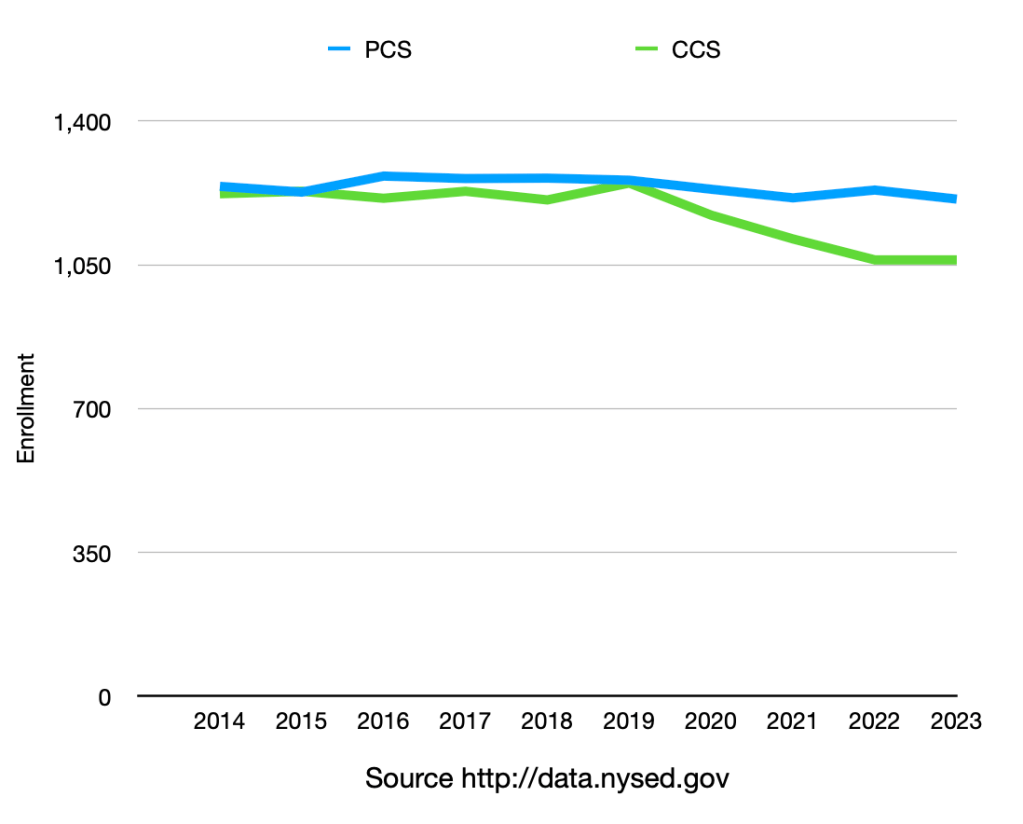

On Tuesday North Country residents vote on next year’s school budgets. One alarming news item reported that Canton Central School district residents are looking at a 6.5% hike in their school tax rates. Why? An article by Jeff Cole in WWNY explains that the primary reason for that increase is declining enrollment. This raises several questions: Did enrollment decline similarly in Potsdam? And why, when enrollment goes down, does the cost of running schools not decline? How long can these levels of increase be sustained?

As discussed in an earlier post, during the last 10 years the population of Potsdam village went down 12% while that of Canton’s rose by 13%. That suggests that PCS must have suffered a similar decline in enrollment, right? But that is not the case. As the NYS Education Department reports, enrollment at PCS has remained steady, averaging close to 1,240 students for the past ten years. Enrollment at CCS, however, averaged 1,225 from 2014-2019 and then started to decline, as shown in the graph below. During the past two years, enrollment at CCS has been 1,062: a decline of over 13%. Why?

Do more retirees live in Canton than in Potsdam? Have the presence of alternative schools, including St Catherine of Siena Academy, Little River Community School and the Deep Root Center started to pull more students out of Canton’s public K-12 system? Or is there a growing trend to homeschool in Canton, as encouraged by organizations like the Christian Fellowship Academy? Whatever the reasons for the enrollment decline at CCS, it results in a real revenue reduction. As all homeowners pay school taxes, not just homeowners with children, the reduction is not due to decreased property tax revenue. Instead, State Aid is tied to enrollment numbers, and State aid amounts to more than 50% of most school’s total revenue.

How great is the reduction in NYS funding to CCS? NYSUT reports that the proposed NYS budget would have resulted in a $613,000 or 4.5% cut in State aid to CCS, while “only” a $189,000 or 1.3% cut in State aid to PCS. This seems to be one reason that residents of the CCS district face a 6.5% increase in their school tax rate and residents of PCS a lower 2.5% hike.

It seems no aspect of public-school financing is reduced when enrollment declines. Why? While buildings may cost the same to service and maintain, would not the costs associated with cafeteria services, bus transport, and insurances be tied to enrollment? Unfortunately, CCS does not provide online, line-item budgets like PCS (PCS’s full 51-page FY25 budget report is available under the Board of Education pulldown menu at potsdam.k12.ny.us ) Looking therefore only at the summary figures reported in the newsletters, we see that school budgets are divided into 3 portions: Program Expenses covering instruction and transport; Administrative Expenses; and Capital Expenses covering the costs of the operation and maintenance of buildings as well as debt services for building and infrastructure upgrades. All 3 sections include employee & fringe benefits for their respective employees.

Keeping in mind that the average rate of inflation last year ran at 4.1%, it is perhaps of interest to see where costs increased the most. Program Expenses at PCS increased 5.4% while these increased 2.5% at CCS as compared to last year. Administrative Expenses increased 8.0% at PCS while they increased 2.4% at CCS. And Capital Expenses increased 27.6% at PCS and a whopping 69.8% at CCS. I cannot ascertain why the Capital Expenses increased so much at CCS (up nearly $3.9 million compared to last year) without a line-item budget report, but I could study the online budget report of PCS. In that budget report we see under the Capital Expense category, the line item for Operation of Plant went up 4.3%; Maintenance of Plant went up 4.0%; Total Fringe Benefits for employees working in the Capital category rose 43.3% or a bit over a quarter million dollars; and the Interest (not the principal) on the Total Debt Payments increased a whopping 235%, from $722,000 to $1,703,000.

How long will schools be able to sustain this level of cost increases? Even without the diminishing enrollment as at CCS, PCS faces massive cost increases for health insurance for employees and retirees as well as pension benefits for retirees, and skyrocketing upgrade costs. This year PCS was able to lessen the tax hike by pulling nearly $3 million out of savings: will we be so lucky next year?

Will I vote for the school budget for PCS on Tuesday? Yes. (If I lived in the CCS district, would I support that budget? Without access to their budget and a report of fund balances and future forecasts, it would be harder to vote yes.) But regardless, it would be great to understand why the costs of running public schools don’t decline with fewer student, and how long we might be able to sustain these levels of cost-increases. Are PCS fund balances able to protect tax payers for a few more years?

post script: I thank Jim Parks for flying me over Potsdam, where I could snap the image of PCS athletic field above.

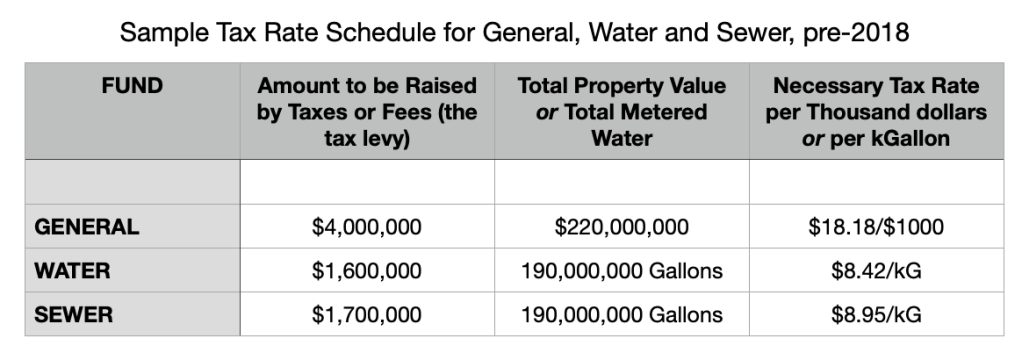

Prior to 2018, the village of Potsdam, like most municipalities, billed for water and sewer according to how many thousand-gallons of water (kGallon) were used per customer. In the sample tax rate schedule below, the tax rates for three funds are presented.

The General Fund, as described in an earlier post, typically needs to raise $4,000,000 from the total taxable property value of the village. The total taxable property value of the village is close to $220 million. So therefore the necessary village property tax rate for every thousand dollars of property value is $4,000,000/$220,000=$18.18

Similarly, the Water Fund might need to raise $1.6 million from water taxes (which are termed water rents). How many total gallons of water are billed for in the village annually? It is close to 190 million gallons. So prior to 2018, to raise the needed water-tax levy of $1.6 million, the water tax rate for every thousand gallons of water had to be set to $1,600,000/190,000kG = $8.42/kG.

Similarly, the Sewer Fund perhaps needed to raise $1.7 million from sewer taxes (termed sewer rents). The number of gallons of sewage generated is assumed to equal the number of gallons of water billed. So the sewer tax rate (sewer rent) required to generate $1.7 million of revenue equals $1,700,000/190,000kG = $8.95/kG. (This information is required, by law, to be published in the budget reports filed on the village website, and is typically found on the second to last page of the documents: see vi.potsdam.ny.us/treasurer )

Everyone more or less understood these things. But the problem the village had was that whenever the water and sewer tax rates were increased (to perhaps pay for some expensive repair or piece of equipment at the water or sewer departments), people would conserve water accordingly, so that their billing remained level. Revenues therefore did not increase and either or both funds went into the red. Frequently.

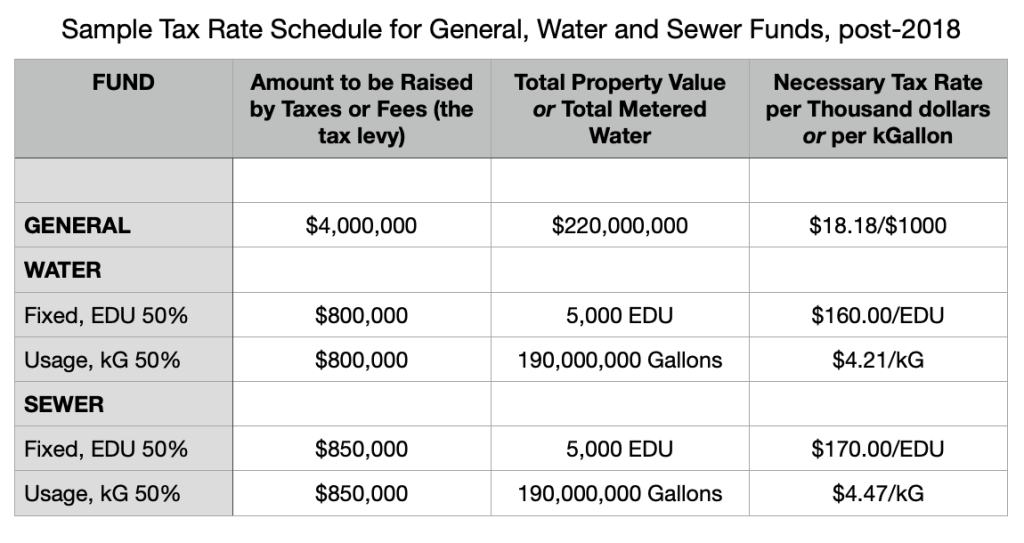

So starting in the early 2000s, municipalities all over the country began to divide their water and sewer billing into a usage portion as well as a fixed portion. Everyone would pay a mandatory, fixed portion, whether they used any water or not, plus a usage portion. This resulted in tax rate schedules like the one below. In the case of our village, 50% of the water (sewer) levy is raised from the fixed portion and 50% is raised from a usage portion. So the tax rates for the usage portions are exactly half their previous rates (the usage levy is 50% of $1.6 million = $800,000 while the total number of gallons of water billed remains at 190 million gallons). But whence the fixed water and sewer tax rates?

Each user (or account) would be assigned an EDU (Equivalent Dwelling Unit) value. Single family homes, for example, all receive an EDU assignment of 1. A two family home receives an EDU assignment of 2. And businesses and nonprofits obtain EDU assignments based on how much water they use: so a laundromat or a car wash would get a higher EDU assignment than a minimart, for example. (One EDU is equal to 120 gallons of water use per day). To see who gets how many EDU, see our online local laws: ecode360.com/attachment/PO0885/PO0885-173a%20Appendix%20A.pdf

Given that the total number of water and sewer EDUs assigned throughout the village is 5000 EDUs, then the water-tax rate required to raise $800,000 is $800,000/5000EDU = $160.00/EDU. Similarly, the sewer-tax rate required in order to raise $850,000 is $850,000/5000EDU = $170.00/EDU.

This would be a good place to end this discussion, but let me continue to itemize my concerns with the system as implemented by our municipality. Businesses, for profit as well as non-profits, have changed their water use significantly over the years (especially during and after Covid), yet their assigned EDUs have never been adjusted. This creates significant inequities. In addition, while water and sewer tax levies have been adjusted, tax rates have not been adjusted accordingly. This makes the accounting of fund balances and encumbrances dubious. Without clear numbers on whether each fund is growing, shrinking or holding steady, the Board can not set prudent tax-rates.

Yesterday, village Trustees received the Preliminary Budget for 2024-2025. The Budget Report is freely available at the village website: vi.potsdam.ny.us/treasurer

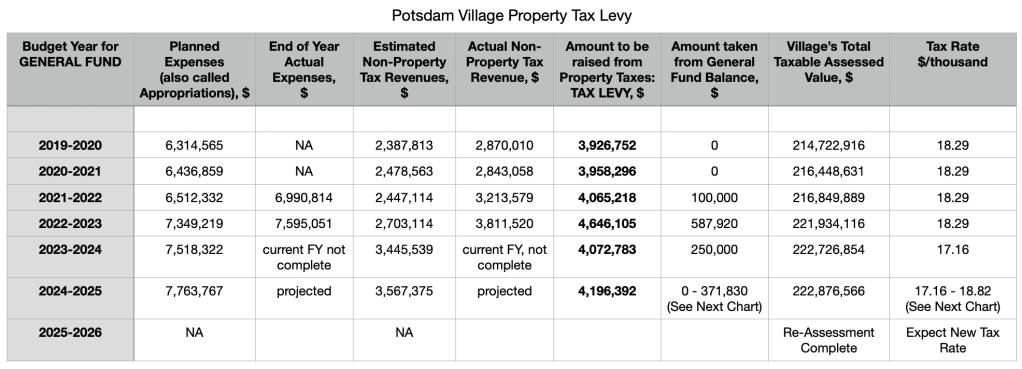

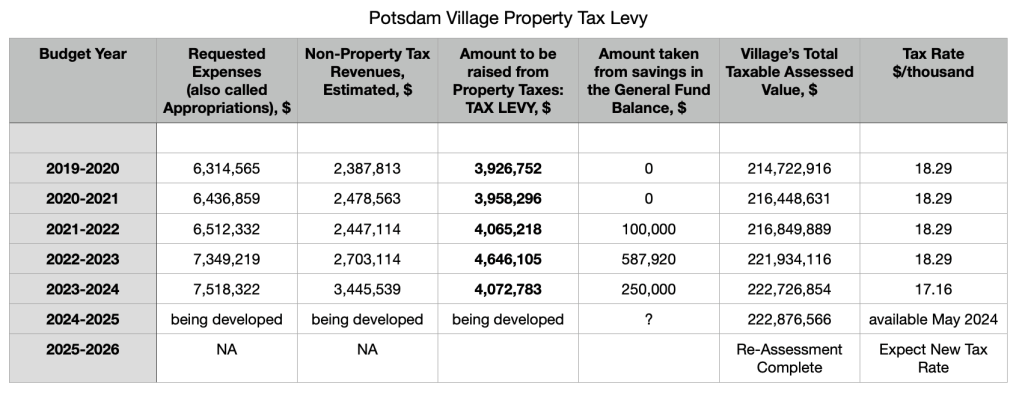

Requisition requests (“Planned Expenses”) for the General Fund amount to $7.8 million for fiscal year 2024-2025, an increase of a quarter million dollars, or 3%, over the previous year’s requisition requests (see chart below). Non-property-tax revenue (primarily sales tax revenue, plus interest earned on savings and income from fees) is estimated to be $3.4 million. Hence the Tax Levy on property, the difference of those two, is $4.2 million, an increase of $124,000 or 3% over the previous year.

What will be the resultant property-tax rate? Will it be $17.16 per thousand dollars in property value, like last year, or will it be $18.29 as during the years 2019-2023, or will it be somewhere in between? That depends on how much the Administration pulls out of savings. Prior to budget year 2021-2022, I can find no instances of money being appropriated from the General Fund balance sheet in order to lower the tax rate (see column “Amount taken from General Fund Balance” above). However, in budget year 2021-2022 a new $3 million loan for a East Hydroelectric Plant rehabilitation became active, requiring either increased tax rates or withdrawals from the General Fund balance sheet.

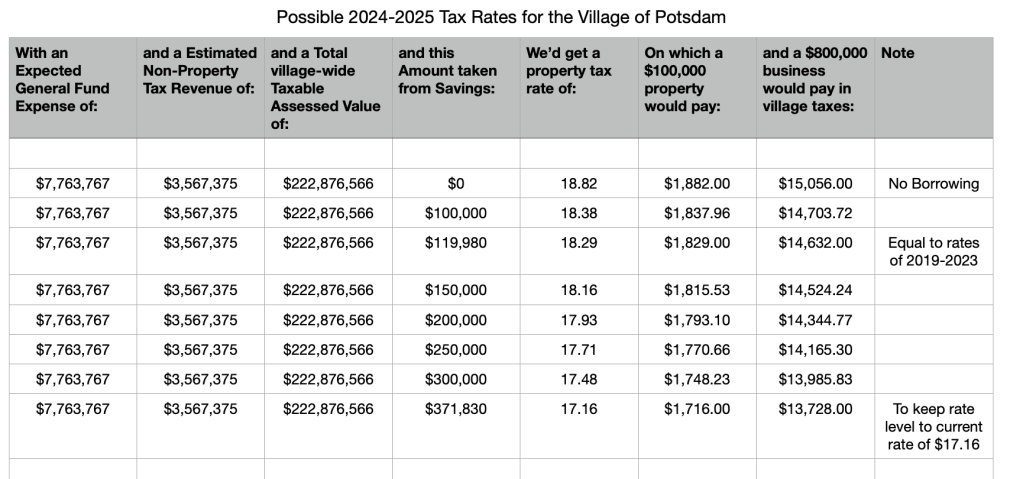

As you see in the chart below for the next budget year, if we do not pull money from savings, our tax rate would be a prohibitive $18.82 per thousand dollars in property value. However, to keep the tax rate at the current level of $17.16, the Administration would need to pull $372,000 out of savings, which also seems imprudent, as the Board does not know the current Fund Balance in the General Fund.

On May 31, 2022 the General Fund held a generous Fund Balance of $4.7 million. The board does not know the General Fund balance since that date, partly because all village revenues, whether into the General Fund, the Water Fund, the Sewer Fund, or from State and Federal grants, goes to the same investment vehicle, and separating which fund held how much is currently only deciphered by our external auditor, not in-house.

As the board begins to deliberate where to set the next year’s property tax rate, it should be noted that (1) the total Planned Expenses, or “Appropriations” at the start of a budget year typically run short of the Actual Expenses at the end of the budget year (see top chart); and (2) Over-spending by the General Fund in recent years has been offset by greater than planned revenues to the General Fund, thanks in large part to increased sales tax revenues and generous interest earned on savings. But both items invite caution: State Comptroller Thomas DiNapoli wrote in a 2/21/2024 press release: “Year-over-year growth in local sales tax collections has slowed significantly, with a nearly flat increase this January compared to last year…With overall growth having moderated over the course of 2023, local officials should remain cautious in their sales tax revenue projections for 2024.” And secondly, if the Administration depletes Fund Balances, the village loses a valuable income stream from interest earned on savings: interest earned the General Fund $250,000 in revenue last year, for example.

The news recently reported that the Potsdam Town Assessor will re-assess the property values of all parcels in the Town of Potsdam, including all Village properties. This is the first re-assessment since 2013. What will happen to our property taxes next year, when the new assessments go into effect? (The new assessments will not affect the tax rate for the upcoming budget year of 2024-2025)

Currently, the village’s Total Taxable Assessed Value is $220 million. My home, for example, has a taxable assessed value of $142,000 (less than its Full Market Value of $169,000 due to tax benefits like STAR). The village property tax-rate is currently set at $17.16 per thousand dollars in property value, so I pay 17.16 x 169 = $2,436.72 in village taxes on my home.

What happens if my home is re-assessed with a 40% increase in its taxable assessed value, from $142,000 to $199,000? Will I end up paying 40% more property taxes: $3,411.41 instead of $2,436.72? This should definitely not happen, under any circumstances. Re-assessments are village-wide, and all properties that have not recently been sold, like mine, will get their Full Market Value re-appraised. (Full Market Values are updated to the sale price of properties on the date of sale.) The upcoming re-assessments might increase the village’s Total Taxable Assessed Value from $220 million to perhaps $320 million (I have zero idea how great the increase will be, this value is merely to demonstrate the process.)

If the re-assessment, including the grievance period, completes before April of 2025, as it is meant to, then the new assessments will dictate the village tax rates starting with budget year 2025-2026. If expenses remain level, for the sake of argument, and the amount of revenue that must be derived from property taxes doesn’t change, but the Total Taxable Assessed Value goes from the current $220 million to $320 million, then the property tax rate would decrease from the current $17.16 per thousand dollars in property value to $11.80 per thousand dollars. That in turn would mean that my current property tax levy of $2,436.72 on my $142,000 home would go to $2,348.2 on my $199,000 home, a slight decrease.

But of course expenses never remain level, and the temptation is great to both lower the tax rate a bit…but not all the way…so as to simultaneously increase the tax levy. So it will be super important to not only keep an eye on the updated assessed values, but equally important to keep an eye on the total Property Tax Levy that the village Board will impose next year. It should not suddenly increase, as this chart makes clear.

As an aside: The Property Tax Levy for the current fiscal year can be located on the village website: https://vi.potsdam.ny.us/category/news/budgets/ Click on Final 2023-2024 Budget. Scroll through to the last page of the document, and you will find the Tax Rate Schedule page for the 2023-2024 tax year. Similar documents for the Tax Rate Schedules of earlier budget years should exist on the village website, but I could not locate them (only truncated budget reports, without Tax Rate Schedule pages). Please visit or call the Clerk or Village Treasurer at 265-7480 for the Tax Rate Schedule for other fiscal years.

Continuing: The chart shows for each of the last 5 budget years the total amount of money requested by the General Fund (“Appropriations”); the estimated non-property tax revenues (including sales tax revenue and building permit revenues etc); and the tax levy, or the amount of money that must be raised by property taxes: this is equal to Requested Expenses minus Non-Property tax Revenue, and has mostly remained close to $4 million per year.

As you see, in some years (especially 2022-2023) the tax levy got too big, and the administration decided to pull sufficient money out of savings to keep the tax rate stable at $18.29 per thousand dollars of property tax. (Last year $250,000 was pulled from savings in order to lower the tax rate to $17.16 per thousand dollars.)

In summary: To determine whether our taxes will change as a result of the upcoming property reassessments, it will be important to keep an eye on the updated property Full Market Values / Taxable Assessed Values, but it will be equally important (if not more important) to keep an eye on the total Property Tax Levy that the village Board will impose next year: The tax levy over the past 5 years has remained around $4,000,000 and should not suddenly rise to $4,500,000 for example.

Between 2010 and 2022 the population of the USA grew by 7.7% while the population of NY State grew by 1.4%. Here in the North Country, however, we have seen a net decline: the population of St Lawrence County dropped 3.7%, from 111,821 in 2010 to 107,733 in 2022. Ominously, the population within the village of Potsdam dropped much more: the village hosted 9,428 residents in 2010 and 8,312 in 2022, a drop of nearly 12%. The population of neighboring Canton Village meanwhile grew by over 13% during those same years! What is the story? Is there a reason people preferentially settle in Canton over Potsdam?

In 2010, the village tax rate in Potsdam was $14.99 per thousand dollars in property value. By 2022 that tax rate had increased by $3.30, to $18.29 per thousand dollars in property value, a whopping 22% increase! What happened in the village of Canton? Their 2010 village tax rate of $10.48 per thousand dollars increased by two cents over the same period, to $10.50 per thousand dollars, a mere 0.2% increase. To put this in context, the 2022 village tax rate of Potsdam was the 8th highest out of 529 villages in NYS, while the average NYS village tax rate was $6.65 per thousand dollars.

Potsdam is a very nice village to live in, but we all must gauge how best to invest and allocate our earnings. Given that the population of Potsdam is shrinking relative to Canton, people are making their preferences known.

During my two+ years on the board, I have heard no discussion on why our tax rates are unusually high nor any discussion on how to lower the rates to make this village competitive with our neighboring towns and villages. Will this year be different?

During the last Fiscal Year (June 1, 2022 – May 31, 2023) the village’s two municipal dams generated $136,201.33 worth of (electric) credit. That sounds like a lot, but the Fiscal Report of 5/31/2023 states that the municipal dams cost the village $533,183.06 during that same FY. The two dams, therefore, generated a revenue shortfall of $396,981.73 during FY23. This nearly $400,000 shortfall is paid for by tax dollars from the General Fund.

By how much do Trustees have to raise the village tax rate to cover a shortfall of $400,000? The village’s total taxable property-value in FY23 was $210,000,000 and the tax rate was $17.16 per thousand dollars of property value. For every $100,000 reduction in appropriation requests (expected expenses), therefore, the board can lower the village tax rate by $0.48 per $1000 of property value. To pay for the shortfall generated by the hydrodams, the board increased the village tax rate by $1.90 per $1000 in property value. For the average village home valued at $104,000 this corresponds to an increased property-tax levy of $198.00 to the homeowner.

The municipal dams have been operating at a loss since at least 2014 in spite of repeated and generous infusions of funds to upgrade performance. In fact, the losses reported by the Hydro Fund have been growing bigger year after year, as new and growing debt payments come due. As of the end of last year, the municipal dams owed the general fund approximately $1,052,122.95. Is it time to try to transfer responsibility and ownership of the municipal dams to an agency specialized in operating these complex machines?

Village homeowners pay taxes that people living in the Town do not:

• A tax based on assessed property value, termed the village tax

• Taxes for the use of water and sewer, termed water and sewer rents

In fiscal year 2022-2023, the village received $4.6 million from property taxes and $3.2 million from water and sewer rents. Together these accounted for 62% of the village’s operating budget of $12.6 million. (A big chunk of the remaining revenue comes from sales-tax revenue.)

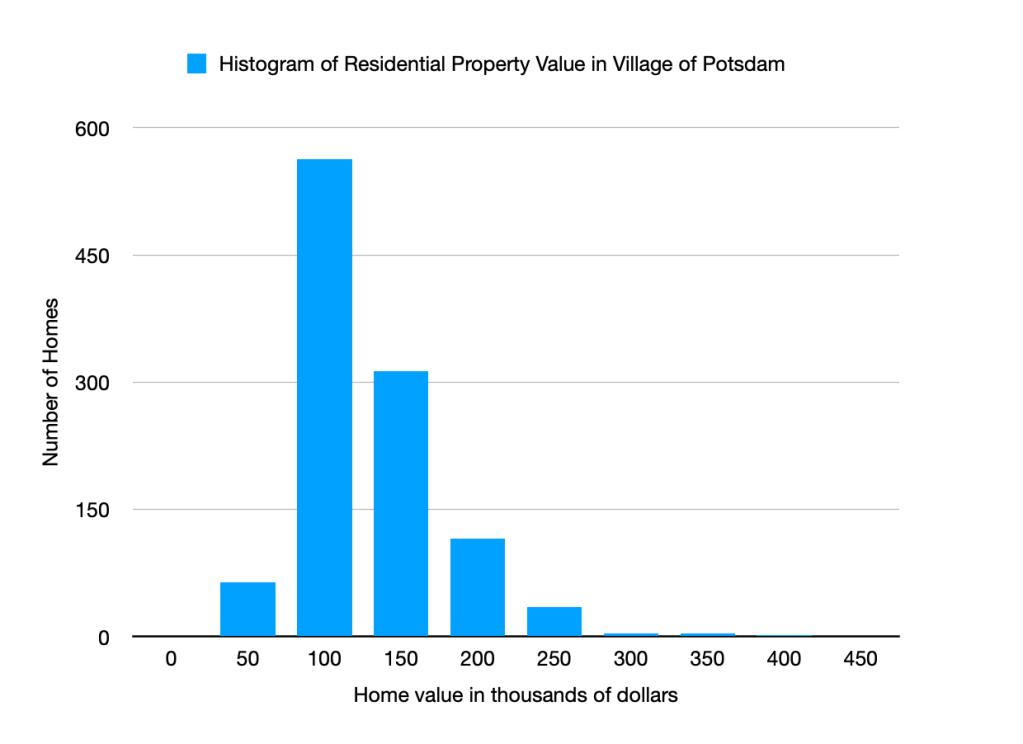

As property tax levies are independent of income, they are considered regressive, not progressive. However, insofar as higher income earners live in properties with higher property values, they somewhat scale with income. This is not true for the sewer and water taxes. Everyone pays the same for those, regardless of income and regardless of the total assessed value of a property. This led me to wonder how property values are distributed in the village.

I asked the Town Assessor for a listing of all residential property values and made the following histogram. There are 1,102 taxable residential parcels in the village, ranging in value from $9,300 to $419,100. The average residential property value is $104,259 while the median home value (the 551st entry of the listing of lowest to highest of all 1,102 entries) is $91,400.

A home with a total assessed value of $75,000 paid $1,371 in village taxes in 2022-2023. If this home stood idle and used no water, the homeowner would still pay $317 in combined water and sewer taxes, which is nearly 1/4 of the village tax amount. In contrast, a home with an assessed value of $220,000 pays $4023 in village taxes and would pay the same $317 for water and sewer rents if no water was used, which represents less than 8% of that homeowner’s village tax.

As trustee, I am asked to supervise the tax levies on village residents. Are the water and the sewer taxes effective and equitable? The taxes were far more equitable pre-2018 when the water and sewer rents were tied to water-usage amounts. Due to the large number of snowbirders and empty apartments, the village often suffered unexpected revenue shortfalls, so the administrator would say the pre-2018 tax structure was not effective. Currently, post-2018, the income stream is stable and effective in that sense, but the tax burden is not distributed equitably. Homeowners who use 5 EDU worth of water, because they empty and fill swimming pools or hot tubs several times a year, pay the same fixed fee as homeowners who use 0.5 EDU worth of water. People who conserve water pay for the profligate users.

Simultaneously, a different burden has been placed on apartment owners. One retiree explained to me that he could not make ends meet financially on his retirement savings and decided to rent out his second floor. This changed his home’s status from a “one-family year-round residence” to a “one-family year-round residence with accessory apartment” and resulted in a 2 EDU-tax for his water and sewer rents (instead of the 1 EDU tax for a one-family residences like mine). Even when his upstairs is unrented, he must pay 2x$317 or $634 in sewer and water taxes annually: over 50% of his village tax. He has been lobbying for a reprieve on this tax burden since 2018.

An apartment complex with 100 units, like Meadow East, uses about 500,000 gallons of water per quarter, or about 2 million gallons per year. Pre-2018 these 2 million gallons cost the owner of the complex $32,040. Post-2018, these same 2 million gallons cost the owner $48,466, a $16,426 or 50% increase. If apartment complexes are set up so each unit is individually metered, as at Swan Landing, this cost is distributed to every renter. In older complexes like Meadow East the apartments are not individually metered, and the owner pays the entire bill. Whether renting out a portion of one’s home as an accessory unit or renting a hundred apartments in a complex, each empty unit costs the owner $317 per year for the water and sewer tax.

In order to create effective, steady income streams for the water and sewer departments, some type of EDU-based billing will be necessary. However, the cost burden should be distributed more equitably so that private and commercial residences do not carry a disproportionate share of the costs.