Water and sewer rates have been adjusted to reward water conservation: If you currently use less than 40 gallons per day (gpd) you will pay less than previous years while if you use more than 40 gpd you will pay more. (40 gpd translates to 1,200 gallons per month or 4,000 gallons per quarter)

I use around 6,000 gallons/quarter so I pay a bit more than last year.

While the rate change encourages water conservation and gives people some control over expenses, it’s likely to create a financial crunch for the village: Most of the water and sewer departments expenses are not tied to water use, but to salaries and debt payments not tied to water use. Expect W/S rates to be adjusted annually as we continue to try to balance the financial constraints of households and businesses against the expense of operating state-of-the-art water and sewer plants.

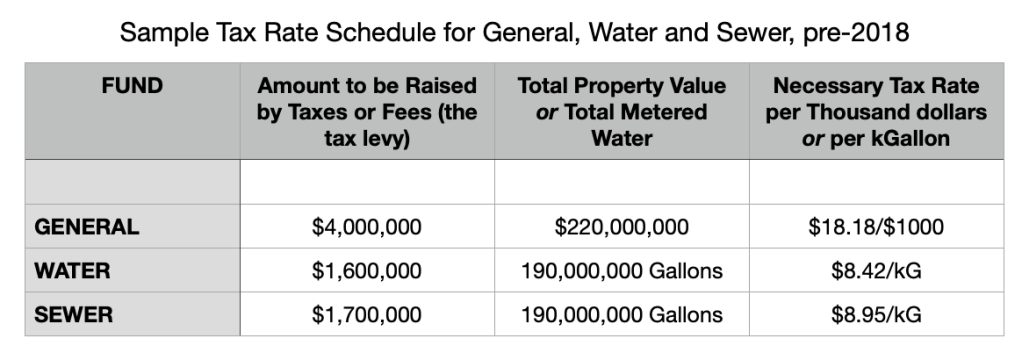

Prior to 2018, the village of Potsdam, like most municipalities, billed for water and sewer according to how many thousand-gallons of water (kGallon) were used per customer. In the sample tax rate schedule below, the tax rates for three funds are presented.

The General Fund, as described in an earlier post, typically needs to raise $4,000,000 from the total taxable property value of the village. The total taxable property value of the village is close to $220 million. So therefore the necessary village property tax rate for every thousand dollars of property value is $4,000,000/$220,000=$18.18

Similarly, the Water Fund might need to raise $1.6 million from water taxes (which are termed water rents). How many total gallons of water are billed for in the village annually? It is close to 190 million gallons. So prior to 2018, to raise the needed water-tax levy of $1.6 million, the water tax rate for every thousand gallons of water had to be set to $1,600,000/190,000kG = $8.42/kG.

Similarly, the Sewer Fund perhaps needed to raise $1.7 million from sewer taxes (termed sewer rents). The number of gallons of sewage generated is assumed to equal the number of gallons of water billed. So the sewer tax rate (sewer rent) required to generate $1.7 million of revenue equals $1,700,000/190,000kG = $8.95/kG. (This information is required, by law, to be published in the budget reports filed on the village website, and is typically found on the second to last page of the documents: see vi.potsdam.ny.us/treasurer )

Everyone more or less understood these things. But the problem the village had was that whenever the water and sewer tax rates were increased (to perhaps pay for some expensive repair or piece of equipment at the water or sewer departments), people would conserve water accordingly, so that their billing remained level. Revenues therefore did not increase and either or both funds went into the red. Frequently.

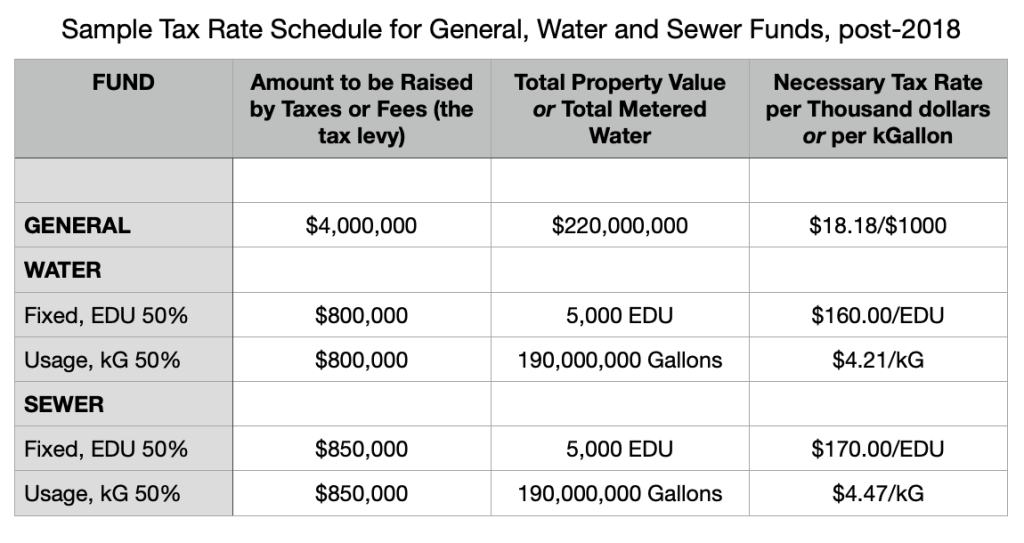

So starting in the early 2000s, municipalities all over the country began to divide their water and sewer billing into a usage portion as well as a fixed portion. Everyone would pay a mandatory, fixed portion, whether they used any water or not, plus a usage portion. This resulted in tax rate schedules like the one below. In the case of our village, 50% of the water (sewer) levy is raised from the fixed portion and 50% is raised from a usage portion. So the tax rates for the usage portions are exactly half their previous rates (the usage levy is 50% of $1.6 million = $800,000 while the total number of gallons of water billed remains at 190 million gallons). But whence the fixed water and sewer tax rates?

Each user (or account) would be assigned an EDU (Equivalent Dwelling Unit) value. Single family homes, for example, all receive an EDU assignment of 1. A two family home receives an EDU assignment of 2. And businesses and nonprofits obtain EDU assignments based on how much water they use: so a laundromat or a car wash would get a higher EDU assignment than a minimart, for example. (One EDU is equal to 120 gallons of water use per day). To see who gets how many EDU, see our online local laws: ecode360.com/attachment/PO0885/PO0885-173a%20Appendix%20A.pdf

Given that the total number of water and sewer EDUs assigned throughout the village is 5000 EDUs, then the water-tax rate required to raise $800,000 is $800,000/5000EDU = $160.00/EDU. Similarly, the sewer-tax rate required in order to raise $850,000 is $850,000/5000EDU = $170.00/EDU.

This would be a good place to end this discussion, but let me continue to itemize my concerns with the system as implemented by our municipality. Businesses, for profit as well as non-profits, have changed their water use significantly over the years (especially during and after Covid), yet their assigned EDUs have never been adjusted. This creates significant inequities. In addition, while water and sewer tax levies have been adjusted, tax rates have not been adjusted accordingly. This makes the accounting of fund balances and encumbrances dubious. Without clear numbers on whether each fund is growing, shrinking or holding steady, the Board can not set prudent tax-rates.

Village homeowners pay taxes that people living in the Town do not:

• A tax based on assessed property value, termed the village tax

• Taxes for the use of water and sewer, termed water and sewer rents

In fiscal year 2022-2023, the village received $4.6 million from property taxes and $3.2 million from water and sewer rents. Together these accounted for 62% of the village’s operating budget of $12.6 million. (A big chunk of the remaining revenue comes from sales-tax revenue.)

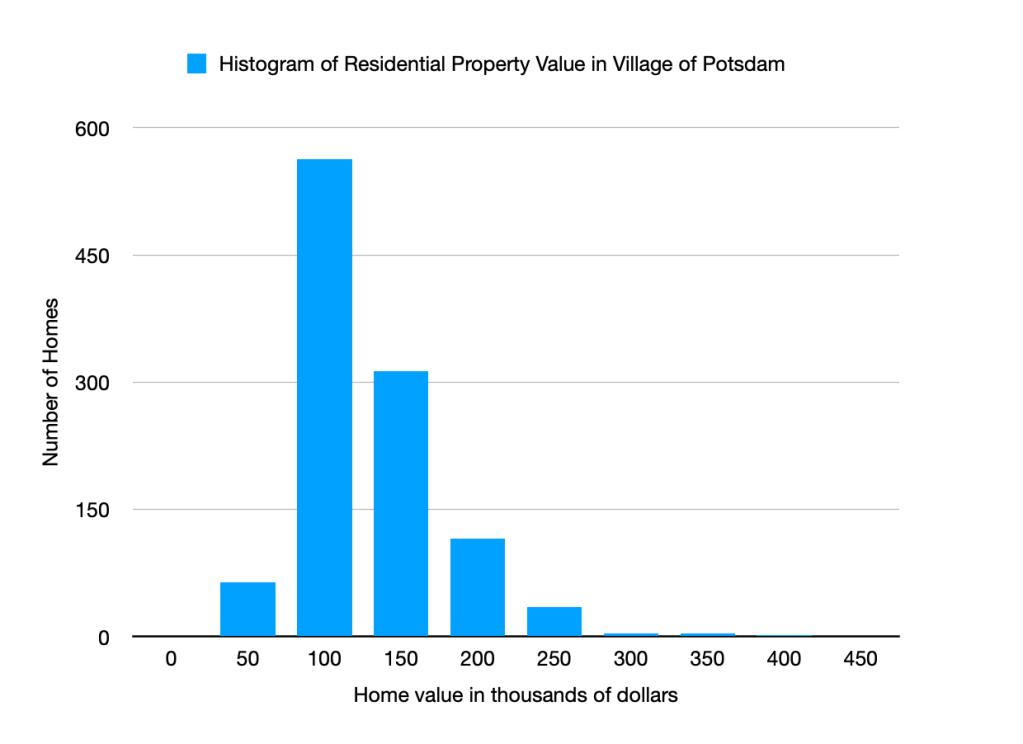

As property tax levies are independent of income, they are considered regressive, not progressive. However, insofar as higher income earners live in properties with higher property values, they somewhat scale with income. This is not true for the sewer and water taxes. Everyone pays the same for those, regardless of income and regardless of the total assessed value of a property. This led me to wonder how property values are distributed in the village.

I asked the Town Assessor for a listing of all residential property values and made the following histogram. There are 1,102 taxable residential parcels in the village, ranging in value from $9,300 to $419,100. The average residential property value is $104,259 while the median home value (the 551st entry of the listing of lowest to highest of all 1,102 entries) is $91,400.

A home with a total assessed value of $75,000 paid $1,371 in village taxes in 2022-2023. If this home stood idle and used no water, the homeowner would still pay $317 in combined water and sewer taxes, which is nearly 1/4 of the village tax amount. In contrast, a home with an assessed value of $220,000 pays $4023 in village taxes and would pay the same $317 for water and sewer rents if no water was used, which represents less than 8% of that homeowner’s village tax.

As trustee, I am asked to supervise the tax levies on village residents. Are the water and the sewer taxes effective and equitable? The taxes were far more equitable pre-2018 when the water and sewer rents were tied to water-usage amounts. Due to the large number of snowbirders and empty apartments, the village often suffered unexpected revenue shortfalls, so the administrator would say the pre-2018 tax structure was not effective. Currently, post-2018, the income stream is stable and effective in that sense, but the tax burden is not distributed equitably. Homeowners who use 5 EDU worth of water, because they empty and fill swimming pools or hot tubs several times a year, pay the same fixed fee as homeowners who use 0.5 EDU worth of water. People who conserve water pay for the profligate users.

Simultaneously, a different burden has been placed on apartment owners. One retiree explained to me that he could not make ends meet financially on his retirement savings and decided to rent out his second floor. This changed his home’s status from a “one-family year-round residence” to a “one-family year-round residence with accessory apartment” and resulted in a 2 EDU-tax for his water and sewer rents (instead of the 1 EDU tax for a one-family residences like mine). Even when his upstairs is unrented, he must pay 2x$317 or $634 in sewer and water taxes annually: over 50% of his village tax. He has been lobbying for a reprieve on this tax burden since 2018.

An apartment complex with 100 units, like Meadow East, uses about 500,000 gallons of water per quarter, or about 2 million gallons per year. Pre-2018 these 2 million gallons cost the owner of the complex $32,040. Post-2018, these same 2 million gallons cost the owner $48,466, a $16,426 or 50% increase. If apartment complexes are set up so each unit is individually metered, as at Swan Landing, this cost is distributed to every renter. In older complexes like Meadow East the apartments are not individually metered, and the owner pays the entire bill. Whether renting out a portion of one’s home as an accessory unit or renting a hundred apartments in a complex, each empty unit costs the owner $317 per year for the water and sewer tax.

In order to create effective, steady income streams for the water and sewer departments, some type of EDU-based billing will be necessary. However, the cost burden should be distributed more equitably so that private and commercial residences do not carry a disproportionate share of the costs.

Money raised from property taxes do not support the operation of the water treatment plant on Raymond St nor the waste water treatment plant on Lower Cherry St. The funds needed to operate, service and maintain the water plant and the sewer plant are raised by user-fees: the water and sewer portions of the quarterly W/S/W bills. Pre-2018 the water and sewer funds routinely ran in the red as predicted revenues failed to match yearly expenses. After the introduction of the EDU-based billing system, the water fund as well as the sewer fund have run profitably with nearly $1.3 million in the water fund and $864,000 in the sewer fund at the end of FY2021 in spite of heavy expenses at the sewer plant.

In 2015, the village board adopted a fund balance policy to maintain at least $250,000 in the water fund as well as $250,000 in the sewer fund. Given that both funds have generously exceeded this since 2019, is it not time to lower the EDU and usage rates? While I welcome a surplus in the water and sewer funds to cover unexpected or anticipated overhauls and updates, the village operates without a multiyear capital plan and without a multiyear financial/strategic plan, which might justify overcharging customers now for anticipated outlays in future.

If inclined, please share your opinion via email or at the Village of Potsdam FB page or in person at the next board meeting (Monday 6 Feb at 6:00 pm)